Introduction

Renting a truck for business purposes can often be a daunting task, filled with the complexities of choosing the right vehicle and understanding insurance options. One key aspect that can significantly ease this process is credit card coverage, particularly when using a Chase credit card. This can translate into substantial cost savings and peace of mind for business owners. With the potential for collision damage waivers, theft protection, and even roadside assistance, understanding how Chase credit cards can guard against unexpected expenses is crucial. Not only does this coverage mitigate risks associated with rental trucks, but it also empowers business owners to operate confidently, knowing they have financial support when it’s needed most. Whether it’s moving equipment or delivering goods, utilizing a Chase credit card for truck rentals can positively impact a business’s bottom line by reducing overall rental costs and improving efficiency.

What is Chase Credit Card Coverage?

Chase credit card coverage for rental trucks is a popular benefit that allows cardholders to protect themselves financially when renting vehicles for personal or business use. However, this coverage often comes with specific limitations and requirements. Here’s a breakdown of what you need to know:

Types of Coverage Offered by Chase Credit Cards:

-

Eligibility: The coverage applies primarily to eligible Chase credit cards, particularly the Chase Sapphire Reserve® and Chase Sapphire Preferred®. To qualify, cardholders must charge the entire rental cost-including taxes and fees-to their card.

-

Collision Damage Waiver (CDW): Cardholders are required to decline the rental company’s CDW to activate their credit card’s insurance benefits. If the CDW is accepted, the Chase coverage is void.

-

Primary vs. Secondary Coverage: Depending on the card type, coverage may be either primary or secondary.

-

Primary Coverage: The card’s coverage kicks in before any other insurance, so it may cover damages without needing personal auto coverage.

-

Secondary Coverage: This kicks in only after your personal auto insurance has been fully used.

Exclusions:

-

Commercial Vehicles: Coverage does not extend to commercial vehicles such as moving trucks (like U-Haul), cargo vans, or large trucks designed for transporting goods.

-

Types of Trucks: Even for personal-use trucks, coverage is limited. Typically, only standard passenger vehicles are covered. If you rent any vehicle classified as a ‘truck’ by the rental agency, it might not be covered.

-

Regional Restrictions: Coverage may not be applicable in certain countries or territories. Always confirm with your credit card issuer to validate your truck rental’s coverage eligibility.

Important Considerations for Business Owners:

- Verify Coverage: It’s imperative for business owners to verify that their specific truck rental qualifies for the coverage before renting. Failure to confirm all requirements can lead to denied claims.

- Read the Fine Print: Understanding the terms and conditions associated with Chase credit card coverage is essential to avoid unexpected costs when renting a truck.

For more insights into vehicle rental options, you can learn more about rental insurance.

This coverage can provide peace of mind, but being aware of the restrictions and requirements can save you a headache later on. Whether you’re moving your business or transporting equipment, understanding Chase credit card coverage for rental trucks is crucial for a seamless experience.

Comparing Chase Credit Card Plans for Rental Truck Coverage

Choosing the right Chase credit card can significantly impact business owners who frequently rent trucks for operational purposes. Here’s a comparative table that details various Chase credit card options along with their rental truck coverage features, benefits, and limitations:

| Chase Credit Card | Coverage Type | Benefits | Limitations |

|---|---|---|---|

| Chase Sapphire Reserve | Primary Rental Coverage | – Covers damage/theft up to $75,000 – Comprehensive travel insurance included |

– Limited to U.S., Canada, and Puerto Rico – No coverage for rentals over 30 days |

| Chase Sapphire Preferred | Primary Rental Coverage | – Covers damage/theft up to $75,000 – Includes additional travel benefits |

– Coverage void if personal insurance claim filed – Limited geographical scope |

| Chase Freedom Unlimited | Primary Rental Coverage | – Covers only damage/theft – No limits on rental period |

– Offers no coverage for loss of use fees – Limited to rentals in the U.S. |

| Chase Ink Business Preferred | Primary Rental Coverage | – Offers strong rewards for business expenses – Covers damage/theft up to $75,000 |

– Must be used for full payment – No coverage for rentals over 30 days |

For more information on specific benefits, you can check out the official Chase credit card benefits page.

Conclusion

When selecting a Chase credit card for rental truck coverage, you should consider not only the primary coverage benefits but also the limitations that may impact your rental experience. For additional insights, feel free to learn more about rental truck insurance on our blog.

Why It’s Important for Business Owners to Understand Credit Card Coverage for Rental Trucks

When it comes to renting trucks, business owners often face decisions regarding insurance coverage that can significantly impact their financial health. One critical aspect to understand is the coverage provided by credit cards, especially for businesses relying on rental trucks for operations such as deliveries, moving, or logistical support. Understanding how credit card coverage works can save money, mitigate risks, and streamline processes.

Cost Savings from Credit Card Coverage

Many business owners may not realize that using certain credit cards can provide substantial savings on rental insurance costs. For instance, most major credit cards, including those from Chase, often include rental truck insurance benefits, which can extend beyond the basic coverage offered by rental companies.

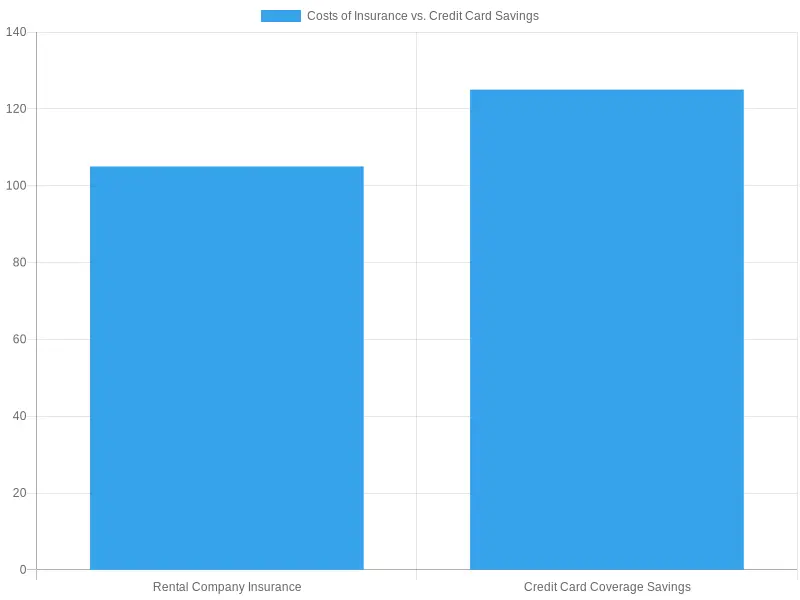

- Example of Savings: When renting a truck, optional Collision Damage Waiver (CDW) offered by rental companies can range from $15 to $30 per day. For a typical 7-day rental, this could lead to a total cost of $105 to $210. By utilizing credit card coverage-if eligible-business owners could avoid most of these fees.

- Illustration of Costs: The cost comparison illustrates that while rental company insurance can add up quickly, credit card coverage can potentially save hundreds on a rental. Here’s a comparison between typical insurance costs from rental companies and the amount covered through credit card benefits:

Mitigating Risks

Not having adequate coverage can lead to significant out-of-pocket expenses, particularly in the event of an accident or truck damage. Without credit card coverage, business owners might find themselves liable for repair costs, which can exceed $10,000 depending on the severity of the damage.

- Risks of Not Having Coverage: If a rental truck sustains damage such as scratches or structural harm, the rental company can charge for repairs and even loss of income due to downtime. Credit card coverage helps mitigate these risks, provided that the regulations and requirements are followed (such as using the card for the payment and declining the rental company’s CDW).

Operational Efficiency

For business owners frequently renting trucks, understanding and leveraging credit card benefits can simplify claims processes and protect against unpredicted liabilities. This streamlining aids in operational efficiency, allowing business owners to focus on their work instead of worrying about potential liabilities associated with rental vehicles.

Key Recommendations for Business Owners

- Verify Coverage: Always check the specifics of your credit card’s rental vehicle policy to ensure it includes coverage for trucks, and note any weight or size limitations that might apply.

- Understand Business Use Exclusions: Confirm that utilizing the truck for business purposes does not invalidate your coverage eligibility.

- Decline Rental Company’s Insurance: Always decline the rental company’s CDW or LDW if using credit card coverage.

- Document Everything: Keep all rental transactions well-documented to support any claims that may arise.

By understanding the nuances of credit card coverage for rental trucks, business owners can navigate their insurance options more effectively, ultimately protecting their bottom line and enhancing their operational efficiency. For more on truck rentals, consider reading about Penske trailer rentals to explore additional options.

Benefits of Using Chase Credit Cards for Rental Trucks

When considering the financial aspects of renting a truck, a Chase credit card can offer some significant benefits. Not only do you earn points on your rental purchases, but you may also enjoy complimentary insurance coverage that can save you considerable amounts in emergencies. An insightful testimonial from a user featured on Reddit highlights this:

“I saved over $100 on my recent move by earning 5x points on the rental charge with my Chase Sapphire Reserve. Plus, the complimentary rental car insurance from the card gave me peace of mind during my long-distance move.”

- Reddit User, r/ChaseCreditCards

This highlights how utilizing a Chase credit card can enhance your rental truck experience while providing financial savings. To delve deeper into other benefits and insights, check out this article on Chase credit card benefits for rental trucks or learn more about how insurance coverage works with Chase cards.

Things to Consider When Renting a Truck

Renting a truck can be a smart solution for business owners on the go, but it’s essential to consider several factors to ensure you choose the right option for your needs. Here’s a checklist that highlights crucial points to keep in mind:

-

Understand Your Needs: Assess what you actually need to transport. Is it equipment, products, or furniture? Choose a truck size accordingly to avoid paying for unnecessary space. Check out this guide on choosing the right truck size.

-

Review Insurance Options: Before signing anything, clarify what insurance is included in the rental. Many business owners do not realize that personal car insurance often doesn’t cover rental trucks. Explore your options for commercial auto insurance or consider coverage available through the rental company, such as Progressive’s guide on rental truck insurance.

-

Compare Rental Fees: Don’t just focus on the base rate. Review all potential fees, including mileage costs, fuel charges, or late return fees. Hidden fees can add up quickly and affect your budget substantially. A detailed comparison can save you money.

-

Inspect the Truck: Always check the truck’s condition before taking it out. Look for any damage or maintenance issues and report them to avoid disputes later. You wouldn’t want to be held responsible for pre-existing issues!

-

Plan Your Route: Map out your intended driving route beforehand. Watch for tolls, restricted areas, or weight limits to ensure a smooth journey. Being unaware can lead to unexpected costs or detours.

-

Check for Specialty Needs: If hauling specific items like vehicles or heavy equipment, ensure the rental company provides the appropriate towing equipment or ramps.

-

Read the Rental Agreement: Lastly, take time to understand the rental agreement fully. Pay attention to mileage limits, fuel policies, and what happens in case of accidents. This will ensure you avoid surprises and fully understand your responsibilities while using the truck.

By considering these factors, business owners can make an informed decision that aligns with their logistical needs and budget. Renting a truck can significantly enhance operational efficiency when approached with diligence and care. For more insights on potential discounts available, check out this resource.

Steps to Ensure Coverage

As a business owner planning to rent a truck, it’s critical to ensure that your Chase credit card offers the necessary coverage. Many credit card holders are unaware of the specifics regarding rental truck insurance. Below are detailed steps to confirm that your Chase credit card covers rental trucks before finalizing your rental:

1. Check your Credit Card Terms

- Review your credit card agreement: Understand what types of vehicles your credit card covers. Most Chase credit cards, including premium options like the Chase Sapphire Reserve® and Chase Sapphire Preferred®, offer insurance primarily for standard rental cars. Coverage for trucks is often limited or explicitly excluded.

- Look for exclusions: Check if there are any specific exclusions related to vehicle type, especially commercial or heavy-duty models.

2. Contact Chase Customer Service

- Ask about coverage for rental trucks: Directly inquire about your specific card’s coverage policy for rental trucks. Clarifying this aspect can prevent issues down the line.

- Verify necessary conditions: Confirm that you need to decline the rental company’s Collision Damage Waiver (CDW) or Loss Damage Waiver (LDW) to activate coverage.

3. Confirm with the Rental Agency

- Inquire about their policies: Different rental companies have different policies regarding the acceptance of credit card insurance for trucks. It’s advisable to ask about their coverage and whether they accept credit card coverage.

- Request written confirmation: Always ask if you can get this information in writing to have evidence of coverage eligibility.

4. Ensure Full Payment with the Card

- Pay the full rental charge with your Chase card: The entire cost, including taxes and fees, must be charged to your credit card for coverage to be activated. Using cash or another payment method may void your coverage.

5. Read the Fine Print Carefully

- Look for detailed terms and conditions: Ensure you clearly understand what your card will and will not cover. Many institutions list conditions that can limit or void your coverage.

- Understand geographical limitations: Coverage can sometimes vary by country or state, so always check if there are restrictions based on your rental location.

6. Checklist for Coverage Confirmation

- Use the following checklist to confirm your Chase credit card coverage before renting:

- Check card terms

- Confirm with agency

- Confirm full payment

- Decline insurance

- Request written confirmation

- Read all the fine print

By following these steps diligently, you can ensure you have the necessary coverage when renting a truck for your business. Remember, understanding your credit card benefits can save you from unexpected expenses or liabilities during your rental period. For more insights on truck rentals, consider exploring our blog section for the best practices on heavy-duty vehicle rentals and policies.

For further information on rental truck options, visit Penske One-Way Truck Rentals and discover how you can ensure a smooth experience in your rentals!

In conclusion, understanding the coverage provided by your Chase credit card when renting a truck is essential for business owners. Chase credit cards offer valuable rental truck insurance benefits, including protection against damage, theft, and loss, which can significantly mitigate financial risks. It is important to note that this coverage is secondary, meaning your personal auto insurance must be exhausted before the benefit kicks in. Additionally, the specific terms and limits vary by card, so verifying the details is crucial to ensure adequate protection. By leveraging your Chase credit card’s rental coverage, you can help safeguard your business investment during vehicular rentals. Don’t forget to explore more about rental truck insurance to better understand your options. If you’re looking for pizza truck solutions to enhance your business offerings, visit truckpizza.net today!

Cost Savings Analysis for Business Owners

Understanding the financial implications of using a Chase credit card for rental trucks can help business owners make informed decisions. Below is a cost savings analysis showing the benefits of utilizing Chase’s coverage compared to traditional rental options.

Cost Comparison

| Description | Cost Without Chase Coverage | Cost With Chase Coverage | Potential Savings |

|---|---|---|---|

| Mid-Size Pickup Truck Rental | $180 | $180 | $0 |

| Collision Damage Waiver (CDW) Fee | $20 | $0 | $20 |

| Total Cost | $200 | $180 | $20 |

Note: The rental cost is estimated at $180 with an additional $20 CDW fee without coverage. By using a Chase credit card, the CDW fee is waived, leading to savings.

Chart Visualization

This chart illustrates the differences in costs effectively.

For more information on rental options, check out our guide on Penske truck rentals or Chase credit card benefits.